1. INTRODUCTION

Since its introduction in 1990s, the broadband technology has witnessed a dramatic diffusion worldwide, and in OECD countries, the average rate of household access to this technology was around 47% by the year 2011, while 76% of individual had wireless broadband technology (Lee et al., 2017).

Broadband technology in the world today is the next phase in internet evolution. In fact, Shin and Koh (2017) assert that the emergence of broadband technology has brought many possibilities to internet users at a faster rate. It is evident that, in the future, internet through broadband would make a big difference in the lives of the public, industry, and the government.

The diffusion of broadband technology is heavily regulated and controlled by the market, government, and consumer. This access controlling policy will lead to the creation of an oligopoly market and threaten the differentiation and quality of services available (Ma and Jia, 2017).

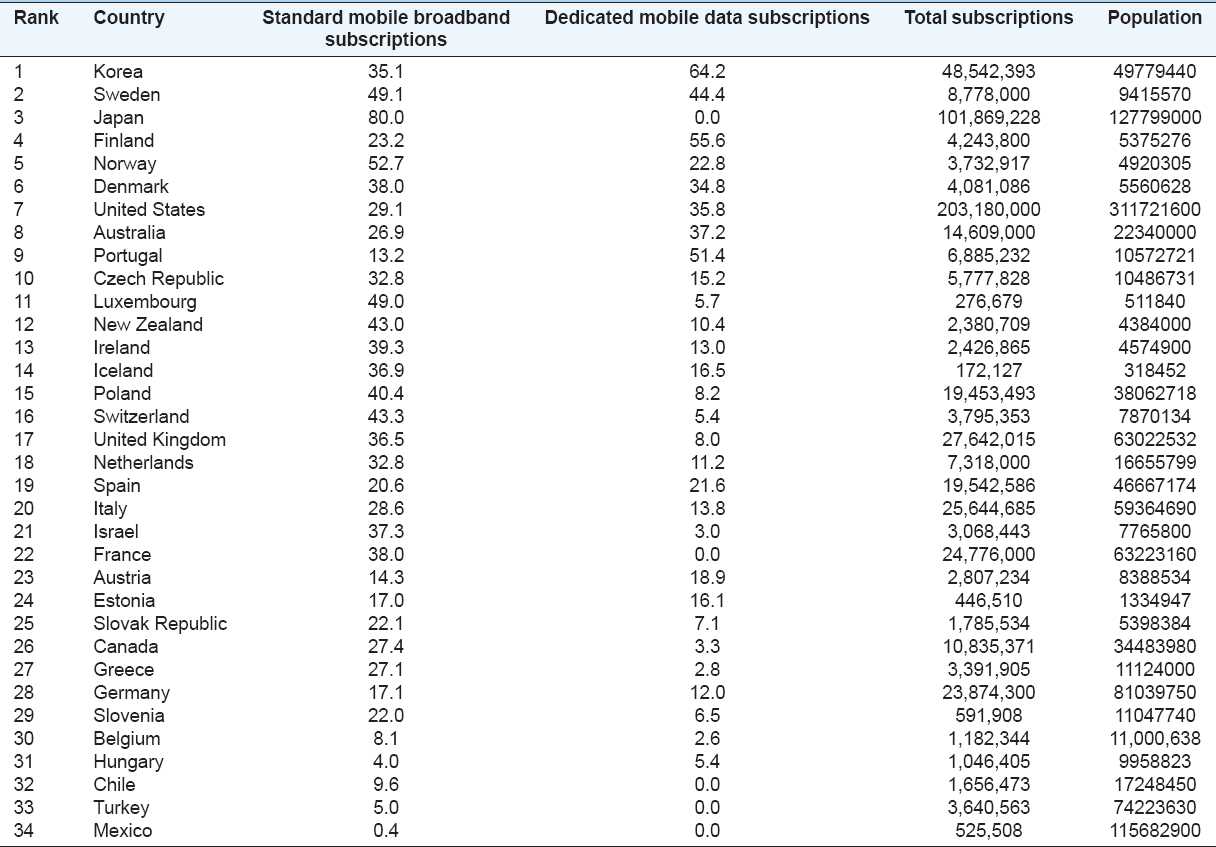

The aim of this study is to make a comparison in the policy regarding the diffusion of broadband in two high-income OECD countries, Sweden and South Korea. One of the countries with the highest broadband penetration rates in Europe is Sweden with speeds of 100 Mbps. It reflects the effectiveness of broadband policies by the government and the rapid adaptation of Swedish people in emerging technologies (Kongaut and Bohlin, 2016). According to the OECD (2011) report, South Korea is the highest country with the access to broadband services, with the total number of 48,542,393 subscribers that accounts for more than 95% of its population, followed by Sweden which has the second highest rate of internet penetration among the OECD countries, with a total number of 8,778,000 subscribers that account for more than 93% of its population [Table 1].

Table 1: OECD broadband subscriptions per 100 inhabitants, June 2011

Table 1 shows the broadband subscription of OECD countries in 2011 along with the population size, the broadband access is divided into standard mobile broadband1 and dedicated mobile data2. Notice that some countries such as Japan and France have zero dedicated mobile subscription in 2011.

On the other hand, South Korea had the highest per capita rate of broadband use [Table 1].

2. LITERATURE REVIEW NETWORK EFFECT AND PLATFORM COMPETITION

One of the most industry factors in the mobile market is the competition factor, in which it has been widely examined in the literature ( for example: Bohlin et al., 2010; Kauffman and Techatassanasoontorn, 2005; Lee and Lee, 2014). It is important for governments to issue policies promoting competition in the broadband market through the reduction of economic barriers to entry so to allow new business entrants to build network infrastructure and collaborate with others for infrastructure sharing (Chapin and Lehr, 2011; Lee et al., 2011).

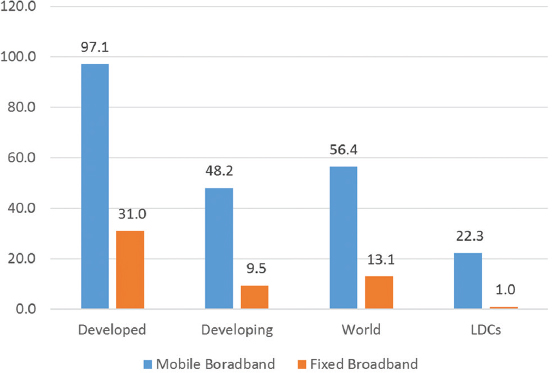

It is argued that broadband and its penetration rate are critical enhancing factors of the economic growth and citizens’ well-being of a country (Figure 1 shows the world’s broadband subscription per 100 people in 2017).

Figure 1. World’s broadband subscription per 100 people, 2017

Source: Adapted from ITU data

By the middle of 2017, according to the International Telecommunication Union estimation, the fixed broadband connections in the least developing countries were just 1 per 100 people compared to 22.3 mobile subscriptions per 100 people. In the developing countries, the broadband technology penetration has been more successful than the developed countries.

By the middle of 2017, mobile broadband penetration was over 5 times higher than fixed broadband penetration in developing countries, while in developing countries, the mobile penetration recorded 3 times higher than the fixed broadband [Figure 1]. Broadband services increase job opportunities and consumer surplus in addition to its effects on gross domestic product (GDP) growth (Lee et al., 2017).

The business trajectory of new technologies such as broadband is influenced by market competition (Lee et al., 2017; Lee et al., 2017). In addition to that completion based on infrastructure type and quality has been developing in different speeds worldwide with some countries enjoying more competitive healthy market than others (Fabritz and Falck, 2013).

One theoretical concept that affects the adoption of broadband technology is network effect. Computer dictionaries commonly define network effect as the increased value of a product as a result of more people using a product. A well-defined network effect is provided by Liebowitz and Margolis (1994) as follows: “The circumstance in which the net value of an action is affected by the number of agents taking equivalent actions.”

Although Sweden as well as the other developed countries such that South Korea benefit from broadband internet services, there are still countries that need more improvement in the deployment of broadband technology. In a cross-country study made by Lee et al. (2011) comparing broadband services among OECD members, it was revealed that developed countries such as “Norway, Denmark, Netherlands, as well as Switzerland” are the ones leading the OECD countries in terms of broadband development. The implementation of broadband is done through digital subscriber line (DSL), fiber to the home, or even cable modem (Baller et al., 2016).

A product may not really become successful because it is faster or cheaper than a competitors’ one but it is suited to the environment. It is compatible to systems as well as the culture of users. Hence, if a consumer chooses a product, she is not the only benefitting from it but other users as well.

Atzori et al. (2010) argued that for products that have network effects, customers base their choice not only on the price nor features of the product but also on the size of the network as well. This is commonly seen in consumers who join a certain network since it is highly popular. Everyone thinks that the popularity is a result of the size of the network. On the contrary, it is the size that creates popularity if according to the authors’ argument.

In relation to this, Varian (1999) asserts that products with network effects grew bigger due to positive feedback. However, the product must have a sizeable base to create a strong feedback system that can create a cycle of increasing base. If old consumers observed that there is an increase of users for a new product (i.e. broadband), they may switch to such product, especially if the product is very accessible and easy to use. People are easily adapting to new technologies nowadays. Using the U.S. state data in 2000, Aron and Burnstein (2003) argued that the independent effect of intermodal competition is has a positive correlation with the increase in households’ subscription to fixed-broadband services.

3. HISTORICAL DEVELOPMENT OF BROADBAND MARKET

3.1. South Korea

South Korea has established a robust national strategy for its broadband technology development that supported politically from its government. It is worth to mention that the Korean Information Infrastructure KII plan which has been adopted by the Ministry of Information and Communication MIC aimed to connect 84% of Korean households to broadband services (Shin and Koh, 2017).

The South Korean government has deployed in addition to the other services, the Broadband Convergence Network BcN and IT839 that aimed to create a ubiquitous network enabling its users to communicate anytime through different technology and devices.

The Korea Telecom (KT) is considered as the incumbent telecommunications operator and the major nationwide local call service carrier in South Korea. KT launched full ADSL services in June 1999. In 2005, KT launched a BcN service for commercial use. At the end of March 2009, South Korea had 46.24 million mobile subscribers.

South Korea is one of the leading countries when it comes to mobile broadband such as 4G/LTE services. By the end of 2008, South Korea had more 16 million internet subscribers. The main mobile operators in South Korea are SK Telecom, KT Freetel (KTF), and LG Telecom. SK Telecom is the main player in the South Korean mobile market with 23.35 million subscribers and a 51% market share. It was one of the first mobile operators to launch commercial services which use CDMA, CDMA 2000x1, CDMA EV-DO, and HSDPA networks providing wireless internet and mobile multimedia services (Point Topic Ltd., 2016).

KTF is the second largest mobile operator in the country with a 32% market share. In June 2009, KTF merged with its main shareholder KT, creating the country’s largest telecom company to offer both mobile and fixed-line services. KTF has a commercial 4G synchronized service and a CDMA 2000 1X EV DO service which can be used anywhere in the world (Point Topic Ltd., 2016).

LG Telecom is the third largest mobile carrier with 8.3 million subscribers and an 18 % market share. The operator came under fire for the slow launch of its 3G services, with the regulator threatening to take away its license. LG Telecom finally launched its 3G network in September 2007. LG Telecom launched a 4G network in 2013 (Point Topic Ltd., 2016).

South Korea recorded 72% improvement in its broadband quality score and rose just above the 2015 broadband quality leader Japan. This improvement is due to continuous support by the government to strengthen the country’s position as one of the world’s ICT leaders. Combined with higher broadband penetration, South Korea rises above Japan in the global broadband leadership rankings (Point Topic Ltd., 2016).

One of the main factors in the rapid development of broadband technology in South Korea is the fierce competition among competitors. Moreover, the competition in Korea is more of “facilities-based” as KT holds 55% of the market (Park et al., 2017). The competition brings down the prices which greatly benefits the general public. In fact, the consumption of broadband is not <60% of the internet population or “netizens” (Lee et al., 2017).

This implies that the market for broadband service in Korea is highly competitive and a fertile ground for making good money. In fact, even the so-called “cyber” apartments or buildings have been wired with optic fiber, as an indicator that Korean inhabitants are serious in acquiring high-speed broadband internet in their households. The Korean government has been very supportive in the thrust toward making Korea advance in technology since it encourages a free market in this field. There are several competitors in the Korean market: Korea Thrunet Co., the first broadband services over proprietary cable infrastructure; Hanaro Telecom, the second largest provider (merged with SKT); and KT, the incumbent operator (Kushida and Oh, 2006).

Moreover, in 1998, the South Korea has started the service of Broadband, at the time, the Thrunet Company introduced the service over the cable infrastructure owned by itself. It is important to mention that Thrunet is established in the year 1996 as a consortium of over one hundred companies under the sponsorship of Dacom (Data Communications Company of Korea), the long-distance competitor to KT, which had entered the market in 1995.

According to Kushida and Oh, 2006, the main shareholder became the state-owned energy company Korea Electronic Power Company (KEPCO), and when Thrunet Company started its service, it used its owned service and rented additional infrastructure from KEPCO. It was surprising when KEPCO had made a wide challenge to build its own fiber-optic infrastructure, without direct support from the government and without authentication. Its eventually the broadband service became quite popular among the South Korean public, impatient with the slow connection speed of dial-up services (Kushida and Oh, 2006).

The beginning era of South Korea’s broadband diffusion was from the entrance of a startup firm (Hanaro) into the market of broadband services. The Hanaro Company was established as a result of the government’s announcement in 1996 for licensing only one competitive company to enter into the local telephone market. KEPCO, chaebol such as Samsung, LG, Daewoo, and Dacom were initial investors, and Shin Yung Shik, former vice minister of Technology and top management of Dacom, was one of the initial leaders.

In an attempt to create a relatively even playing field, the Ministry of Information and Communication created a new set of regulations that prohibited KT from subsidizing its local service, with profits derived from its long distance or international operations (Kushida and Oh, 2006).

Hanaro discover that, after the entry of the local telephone service market, it cannot easily compete against KT, the latter had the capability to offer high-quality service for minimum prices that cannot be competing by Hanaro, eventually, the lack of number of portability triggered Hanaro to face network effects (consumers facing switching costs, this will for sure keep them tied to KT’s service).

Hanaro eventually faces a distraction when its customers’ surveys showed that KT’s data service subscribers such as dial-up mode and Integrated Services Digital Network.Internet service has blocked many complaints, especially, that the speed was slow, and the price charge was per minute based. DSL technology, which utilized existing copper infrastructure, delivered higher speed, and could be offered at flat rate fees, provided an opportunity Hanaro could not pass up and sustain in the market (Kushida and Oh, 2006).

Furthermore, the market segment and the regulatory framework lead the Hanaro to start offer the DSL service as the internet service provision (ISP) was somehow unregulated segment of the market, it was not required authentication and licensing. Furthermore, in 1997, the government had switched from a positive list system, allowing only government specified activities by service providers, to a negative list system, in which service providers could provide any service except government prohibited ones.

Therefore, as a consequence, in April 1999, Hanaro started offering broadband services, operating both DSL and cable, using its own DSL network, and leasing cable capacity from a subsidiary of KEPCO and KT. With its entry into broadband service, Hanaro started its aggressive competition and established a price-free business model, by providing the broadband service as a free addition to its basic telephone subscription, which amounted to $40 with free installation. This price-free business model has aided Hanaro in successfully gaining more than a million subscribers within 18 months of introducing its DSL service (Kushida and Oh, 2006).

This success of Hanaro in DSL service business has affected the performance of KT, the foremost incumbent carrier. KT was investing mainly in ISDN, the success of Hanaro business leads KT to think about investing in more services, especially in DSL taking advantage from that the users were preferring its high-speed flat-rate low subscription price, and high sustainability service of internet access. As a result, in 1999, KT has launched the DSL service, competition further heated up when other firms, including SK Telecom in 1999 and Onse Telecom in 2000, also entered the market.

Furthermore, the DSL service offered by Hanaro was only covering Seoul and some major cities in South Korea, this motivated KT to offer DSL service in all over the country. KT’s competitive pricing and rising demand for broadband enabled it to quickly catch up and surpass Hanaro’s market share by June 2000, retaining a dominant market.

One can realize from the South Korea’s industrial policies for broadband and within its strategic liberalization drive, its attempt to not only enhance supply-side investment in networks, but also to promote demand for use as well. In its classical developmental strategy, South Korea is usually considered to have been a producer rather than consumer-oriented, channelling peoples’ income into relatively centralized banking systems, by keeping individual access to other avenues of investment such as securities or offshore markets relatively difficult, and then channelling those savings into strategic sectors. The KII strategies fall in the line of this classical industrial policy.

3.1.1. Korea Thrunet Co., Ltd

One of the largest and leading telephone companies in South Korea is Korea Thrunet Co., Ltd., which is based in Seoul. One of its divisions is Multi Plus which handles a big percentage of the internet market in South Korea. The first Korean company which offered the broadband internet access services was Thrunet, in 1998, it had the largest cable network subscriber. It is important to mention that Hanaro Telecom acquired Thrunet in 2005 (Ueda et al., 2006).

3.1.2. Hanaro Telecom

Another key player in the industry is Hanaro Telecom Inc. This company is fast-rising as it provides high-speed internet service since its inception in September 1997. In fact, this company was responsible for launching of the first ADSL service a decade ago. Hanaro Telecom was providing service to Seoul, Busan, Incheon, and Ulsan at the head of the list by April 1999. Hanaro expanded the internet access market by developing nationwide fiber-optic networks to 100 cities by the end of 2002 (Ueda et al., 2006).

It is worth mentioning that Hanaro strongly pushed DSL broadband service. There were many factors that can be attributed to the success of this company. However, the most important attributable factor is its marketing strategy that it focused on building a good brand image to the Korean market. The company also believed that if it pursues its expansion, customers would eventually follow. Currently, the company has a prepaid subscription so that supply can be monitored (Ueda et al., 2006).

3.1.3. KT

KT is known for its world class technology for the past 25 years. It has been the leader in the telecommunication industry as it provides a combination of wireless/wired communication. This company has contributed to making into a phenomenal IT success because of its broadband technology. Its wireless broadband service (Wibro) is a first in the world’s wireless broadband technology. The website KT presents it’s as an umbrella corporation which has the companies: KT, KTF, KITCOM, and KTH (Kushida and Oh, 2006).

As early as 1997, this company had already offered ADSL services. At that time, it was quite costly to offer it since the equipment alone costs a lot of money. The only solution then was to get a multitude of subscribers not less than half a million who were willing to pay 50–60 USD per month for service. The business case for ISDN at the time appeared much stronger.

However, two new entrants were then successfully launching, Thrunet and Hanaro, which persuaded KT to discuss its plan to roll out ISDN and to offer commercial ADSL services at its competitor’s price of 30 USD per customer or 9.0% less than this company’s original price. KT just used its own existing network and gained around 2 million subscribers in a year’s time, thereby cutting the price by 50% and dominating the competition (Kushida and Oh, 2006; Ueda et al., 2006).

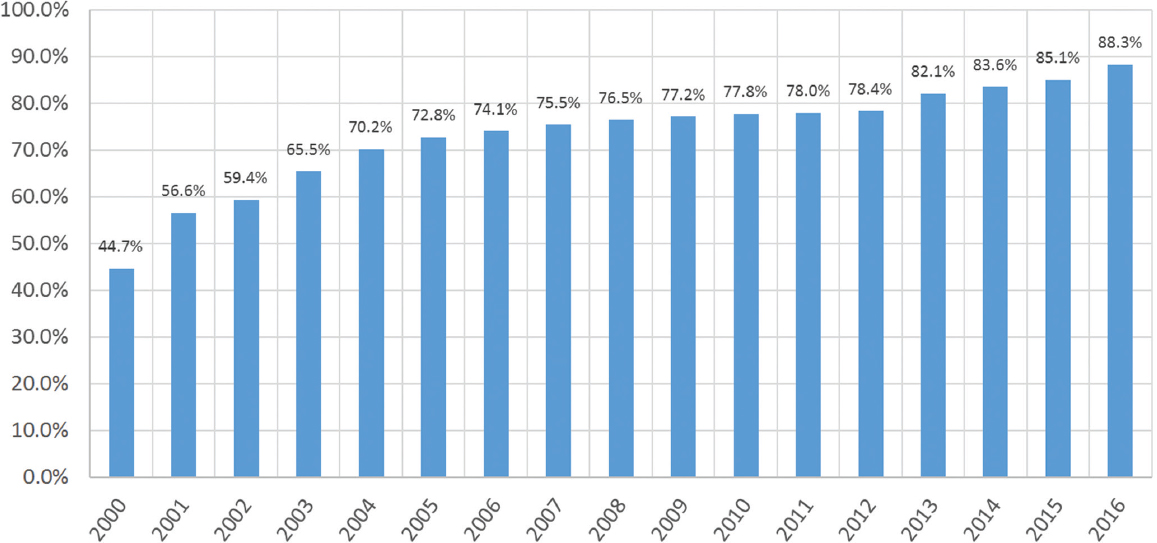

Figure 2 shows the share of Korean population with home internet access, notice that since the year 2000 the share of home internet access has been increased to reach more than 83% of the population.

Figure 2. Share of Korean population with home internet access

Source: https://www.statista.com/statistics/226712/internet-penetration-in-south-korea-since-2000/

3.2. The Swedish Broadband

Before 1993, the Swedish government owned Televerket which was mainly of a public voice telecommunications provider in countrywide. In 1993, the Swedish state converted Televerket into a government-owned utility and renamed it as Telia AB; moreover, 30% of its shares were sold to the public initially in June 2000 (Point Topic Ltd., 2016).

Later in 2002, Telia AB merged with TelcoSonera from Finland, thereby creating TeliaSonera. This merger became a leading telecommunications group that covered the Nordic and Baltic regions as well as Eurasia. Currently, the Swedish government holds a 37.3% share in the company after selling it to institutional investors. By 2008, these investors owned 24.2% of the shares in the company.

At that time too, the IP-based subscriptions increased while fixed telephone subscriptions decreased in Sweden. As of the past year, the IP-based subscriptions increased by 31% which manifests the consumers desire to transfer to IP telephony (Point Topic Ltd., 2016).

Nevertheless, TeliaSonera is still the largest telecommunication company in Sweden followed by Tele2, Comhem, and Bredbandsbolaget. Even in the mobile market, TeliaSonera continues to dominate with a share no close to 40%. It also acquired a 4G license in May 2008. By the next year (2010), this company aims to provide “mobile broadband services with over 100 Mbps speeds” (Point Topic Ltd., 2016).

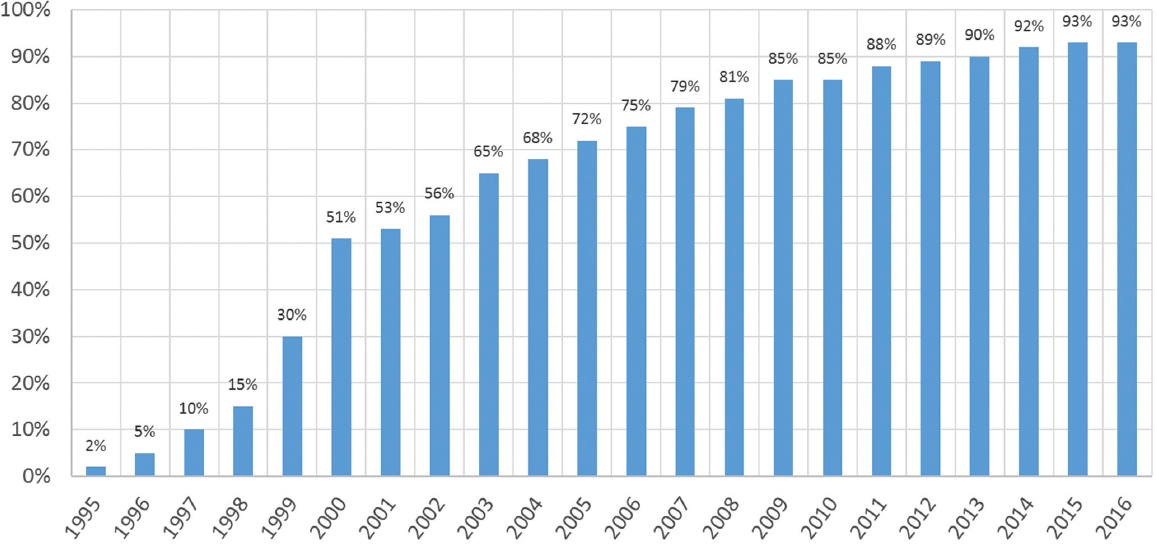

In terms of broadband users in the country, in the year 2016, 93% of the population in Sweden has internet access at home3 [Figure 2]. The total number of broadband subscriptions has increased sharply in recent years, principally as a result of the strong growth in wireless broadband and fiber LAN.

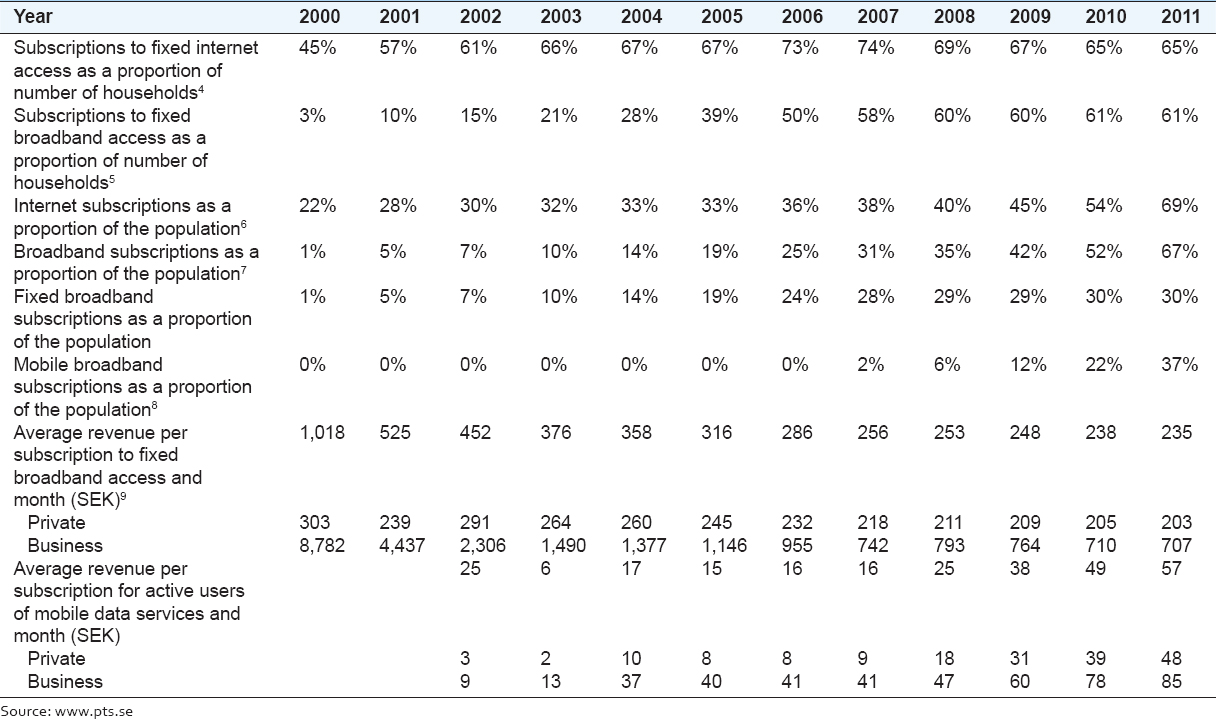

By the end of year 2011, the total number of subscription to broadband access was 61%, in which it accounts for 67% of Swedish total population [Table 2]. The average revenue per subscription to fixed broadband access and month was 235 million SEK.

Table 2: Internet services growth, penetration, and average revenue in Sweden

Figure 3 shows the number of Swedish households using the home internet in which it has been dramatically increased from the past two decades to reach 93% by the year 2016.

Figure 3. Share of Swedish population with home internet access

Source: https://www.statista.com/statistics/543324/sweden-access-to-the-internet/

4. GOVERNMENT POLICY FOR BROADBAND DEPLOYMENT

4.1. Sweden

The country of Sweden is one of the leading countries with regard to IT usage and broadband penetration. The country maintains its top ranking position according to Economist Intelligence Unit, World Economic Forum, and in the EU’s Broadband Performance Index (Stenfeldt and Andersson, 2016).

Sweden has a strong IT and telecommunication sector and an extensive investment in research and development, and its innovative capabilities made it possible to produce new services, products and leading companies, modern mobile telephone such as NMT and GSM were invented and developed.

A high proportion of the labor force and skilled labor are employed in the IT sector or IT-related jobs in other industrial sectors. The IT sector also strengthens other main industries in Sweden, such as the automotive, pharmaceutical, and engineering industry (Stenfeldt and Andersson, 2016).

The government of Sweden known as Riksdag (Parliament) has agreed through its Broadband Strategy that the primary purpose of IT policy in Sweden is “to make Sweden the first country in the world to be an information society for all.” This objective is part of the 2012 IT Bill. In the aforementioned bill, there have been three priority areas for the Swedish government. The Swedish Broadband Strategy’s main focus is as follows:

-

• Building confidence in IT.

-

• Competence in the use of IT - this is done through continuous improvement in the field of IT. However, improvement is not only meant for specialists but also for common people too.

-

• Accessibility to the services of the information society.

Given this focus, there is a great responsibility in the implementation of such goals, namely, in the area of digital infrastructure and education. For one, Sweden is sparsely populated compared to other European countries such as Germany. This translates to bigger investment costs for the government (Kongaut and Bohlin, 2016).

4.1.1. Sweden’s policy on infrastructure and development

The 2012 IT Bill of Sweden’s main theme was “An information society for all.” This translated to provide accessibility to high broadband capacity for all households and businesses in Sweden. In view of this, the government was responsible for implementing measures that assured quick expansion of broadband infrastructure even among rural areas that were sparsely populated. Due to this situation, local and regional authorities played a crucial role in the facilitation of the expanding infrastructure (Brown, 2017).

4.1.2. Participation of regional and local authorities

The Swedish government can provide a subsidy to network builders that belong to the private sector; however, local and regional authorities have been authorized to administer the subsidy since private contractors were not interested. The funds for the project go through a public procurement process as soon as municipalities commit to building the infrastructure themselves (Lucchi et al., 2017).

This idea became very popular to the 289 municipalities of Sweden. In fact, even small municipalities got involved in the creation of their IT infrastructure which was a logical move since only they themselves can answer the needs and demands of their demography.

The applications for subsidies are handled by the County Administrative Boards that carefully inspect the local IT infrastructure program presented by a certain municipality. One of the requirements of the said program is to locate strategic urban centers or areas which can contribute to regional development. There have been hundreds of applications received by the Country Administrative Boards resulting to the usage of 10% of the funding according to the Sweden Broadband Strategy report. This financial support extended continued up to 2005 (Sutherland, 2017).

4.1.3. Infrastructure support

The Swedish Broadband Strategy reported that the government compelled the National Electricity Grid Authority “to hang optic fiber lines on top of their high-voltage poles and towers, forming a backbone broadband network” (p.4). Unfortunately, the market was weak then thus the National Grid fell short of its objectives. Nevertheless, the Riksdag decided to allocate EUR 40 million (part of the 525 million) so that the goal of strengthening the infrastructure would push through (Beckert, 2017).

4.1.4. The regional networks

The government granted EUR 190 million to the networks primarily responsible for connecting the urban centers. This amount equates to around 30% of the total cost spent for that network alone. The main objective of this network is to create a link to each municipality urban canter that has small towns and villages. Through this effort, networks can then be bought, built, or rented out, thereby attracting small network operators (Gerli et al., 2017).

4.1.5. Local networks

Municipalities receive a subsidy for building up local networks, i.e. inside towns or in specific areas in the countryside. Total support will amount to EUR 120 million. This corresponds to a few percent of the total cost for that part of the network.

Approximately, the same qualifying requirements exist for this support as for the regional network mentioned above. The most important difference, however, is that this network should, as a rule, be new. However, in rare cases, the upgrading of existing infrastructure, such as an old telephone access network, for example, for the purpose of an ADSL connection, also qualifies for support (Stenfeldt and Andersson, 2016).

4.1.6. ICT policy in Sweden

A number of points can be noted in the history of ICT policy in Sweden, first: Lack of comprehensive ICT policy document or a specific government department or office that has the responsibility for an overall ICT policy. Policies on trade and industry, education, health, employment, and other sectors comprise of statements mentioning ICT goals, objectives, initiatives, and regulatory measures. The point to mention is that whether this is an effective way of addressing the potential of ICT, or a more comprehensive policy instruments may have better effectiveness and remains controversial.

Second: It made it difficult for firms to make proper strategic plans regarding ICT industries. Over the years, the Swedish government rather than facilitating the development of a competitive industry, it has remained unchanged and no explicit policies were driven.

Third: On several occasions, there has been a conflict between commercial logic and national logic. For example, the case of ICL: It would have made more commercial sense to merge with Fujitsu, rather than with Siemens, as the aspirations of the regional development of the European Union suggested (Ministry of Enterprise Energy and Communications, 2011).

Finally, it is important to understand the influence of particular vested interests in shaping policy initiatives in ICT.

The government continues to rely on competition for both technology infrastructure and information content, and its regulatory role aims at maintaining the free market environment. However, this policy is probed by those who feel that the development of an infrastructure for a democratic information society “the information superhighway” needs more intervene from the government to ensure that the necessary common knowledge is available to all.

Moreover, ICT policy initiatives cannot be understood without knowing the historical context of the society that gave rise to them. Hence, they should not be considered as technical/rational interventions but as the outcome of political tensions and vested interests.

4.2. South Korea

For the promotion of network infrastructure built-outs, the Ministry of Information and Communication has started to use a new acquired resources and policy tools. For example, in the year 1995, the Korea Information Infrastructure Initiative KII has started, which covered in different backbone building and Research and Development Facilitation program, The Ministry of Communication and Information has offered direct subsidy such as financial supports, granting privileges tax holiday, and directly underwrote loans to the internet service providers’ ISPs for building their networks. The government subsidy of equipment purchases, consistent deregulation, and the implementation of market principles led to South Korea possessing one of the most liberalized telecommunications markets in Asia (Kushida and Oh, 2006; Lee et al., 2017; Ueda et al., 2006).

The government’s emphasis on backbone networks as the foundation of its broadband strategy has resulted in a massive development of broadband in rural areas. As a consequence, this policy has reduced costs for broadband providers by accessing subscribers in rural areas without building additional network infrastructure. As a condition of privatization, the KT has legally required to provide a universal service, including a requirement to provide broadband access to rural areas (Ma and Jia, 2017).

In promoting broadband and the internet, the South Korean government enacted a series of demand magnification programs. Different types of programs were designed to facilitate internet education, computer use in schools, homes, to offer computer purchase assistance, and even to educate housewives, who tend to control household finances.

Perhaps, the most clever demand magnification policy was too deeply embed computer literacy in Korea’s ultra-competitive university entrance examinations, making a home PC a prerequisite for any serious education-minded parent, of which there is no shortage as evidenced by the extensive cram school industry (Kushida and Oh, 2006).

Broadband access became a part of the package of computer literacy, driving sales for households with school-age children. While the effectiveness of these programs and policies in promoting broadband cannot be determined decisively, it is noteworthy that the government adopted a range of demand magnification industrial policies in addition to the usual supply-side facilitation measures (Kushida and Oh, 2006).

4.3. Industrial Factors Affect the Broadband Development

Industry factors such as fixed broadband price, speed, bandwidth, and telecommunication infrastructure may have effects on the rate of fixed broadband penetration. Through statistical analysis of approximately 100 countries, Martha (2005) found that factors such as price, income (measure by GDP per capita), and competition are affecting fixed broadband adoption.

Cava-Ferreruela and Alabau-Munoz (2006) found that technological competition, low cost of deploying infrastructures, and prediction of the use of new technologies are considered as key factors for broadband supply and demand. Fransman (2006) suggested disruptive competitors which construct market share through “below-cost” pricing determine the global broadband performance.

In a study conducted by de Ridder (2007), it is showed that the price of low fixed broadband is associated with the high level of broadband diffusion. Atkinson et al. (2008) also found that the price of low fixed broadband is a factor of broadband adoption in OECD countries. More recently and by employing multivariate data analysis of 110 countries, Brown et al. (2017) found that broadband speed, platform competition, and content are the key factors to enhance the adoption of global broadband.

The higher bandwidth technology also increases the rate of broadband adoption. The increase in the demand for higher bandwidth is a key driver of broadband diffusion (Baller et al., 2016).

Fransman (2006) suggests that the capacity of broadband is a measure of national performance in broadband. However, in spite of bandwidth importance as a key determinant of internet adoption, there is no empirical work investigating the correlations between bandwidth and broadband penetration.

5. CONCLUSION

5.1. Challenges for Future development

Although the rate of access to broadband technology is increasing in steady state, the market is continually changing to cope with the rapid development of technology. This trend is driven among other things by different factors that may affect the shape of the market for broadband and other telecommunication technologies. For example, increase in the demand and supply for higher speed broadband accesses to offer and benefits from new and more demanding services that need internet access.

As a consequence, the traffic volume will grow as users spend more time using the internet and more data are transferred between individual, software, and applications. Moreover, the demand for mobile access to the internet will increase as well as demand for more reliable internet connection to cope with the global business that needs access to services anytime and anywhere.

Finally, the market will seek efficiency in terms of cost in which it allows the service operators to produce their services in more cost-saving way, as new technology tends to be more resource efficient.

5.2. ICT Policy Objectives

A number of objectives as stated by Labelle (2005) are necessary to adopt appropriate ICT policy initiatives, and these objectives are summarized as follows:

First: Nationalism/Regionalism in the face of a high technology future is necessary to ensure nation/region retains its national ICT business firms even if they are not competitive.

Second: Geopolitics factors to ensure the state’s military power and the state’s culture preservation/dominance.

Third: The national innovation system as an engine for growth and power.

Forth: The national authority in the face of economic globalization to limit the dominance effects of multinational corporations.

Fifth: Promoting the rational use and enhancing technical and organizational innovation as drivers of efficient national economic development.

Sixth: Cope with the social changes that may exploit the adoption of technology, for example, in education, health care, labor markets, and transport sectors.

Seventh: The development of good infrastructures in different sectors such as telecommunications, education, and government’s regularity framework for free market economic system.

Eighth: Redistribution of profits come from the use of ICT across the population.

Ninth: Adoption of new and use of ICT services by the government.

5.3. Government Policy and Regulation

From the literature, one can explore and notice the differences of approaches adopted by governments and regularity agencies toward the IT convergence. Western countries favor the laissez-faire market approach which advocates for the free market. In contrast, markets in Asian countries, for example, South Korea are led by the government’s national plan with quantified objectives and the regulator’s instrument strategies to meet the mentioned objectives.

Deterministic national plans led by government are not favored by western countries for different reasons. Some critics still equate them to totalitarian approaches with 5 and 10 year strategic plans, and their argument is that they are too dogmatic to enhance the nations’ innovation capabilities (Khayyat and Lee, 2015).

On the other hand, the approach taken by the Asian countries with 5-year digital economy plans has been proved to achieve better results. The reason is possibly due to the importance of convergent network contents and services are no longer questioned, and ICT technology is widely accepted as a major driver engine for economic development.