1. INTRODUCTION

Developments in the macroeconomic environment have become increasingly significant within the agricultural sector. This can be attributed to the fact that the sector has become more capitalized and relies more on international markets, which makes it more vulnerable to macroeconomic fundamentals including changes in interest rates, exchange rates, and international growth rates (Eyo, 2008). Consequently, since the mid-1970s, a number of theoretical and empirical studies have analyzed the impact of macroeconomic variables on the relative performance of the agricultural sector.

Over time, the Nigerian economy has been mainly dependent on oil. However, due to rising inflation, exchange rate crunch, and decline in output, triggered mostly by the global oil price crash and drastic drop in the country’s oil production, the country plunged into economic crisis (Opurum, 2018). As a result, the need to diversify the economy away from oil revenue to agriculture has been one of the major issues that have taken a center stage in Nigeria’s contemporary economic discourse.

The renewed call for diversification in recent times and its link to agriculture underscore the expected role that the agricultural sector and its value chain components are expected to play in attuning the country’s production and foreign exchange earnings to the non-oil sector. Lawal (2011) maintained that the prospects of non-oil subsector and the overall economy of Nigeria are usually tied to the performance of the agricultural sector. Oji-Okoro (2011) posited that over 70% of the active labor force in Nigeria is in the agricultural sector with 88% of non-oil foreign exchange earnings. In addition, approximately 70% of the population engages in agricultural production at a subsistence level (National Bureau of Statistics, 2010). Thus, an intellectual searchlight on agricultural value chain is imperative for Nigeria in an attempt to diversify its economy, reduce the level of unemployment, and protect the value of its currency, and above all improve the living standards of its over 180 million citizens.

Many people in developing countries, Nigeria inclusive, live in rural areas, and the main occupation is agriculture. It is known that the agricultural sector contributes substantially to national income and economic growth, despite the rising trends toward urbanization. The imperatives of agricultural value chains, therefore, lie in the significance of the agricultural sector for economic development, especially for developing countries, majority of whose citizens face various degrees of poverty and are engaged in agriculture. The macroeconomic objective of poverty reduction, for example, can be said to be well orchestrated if it is targeted to improve agricultural value chain, as this will directly impact the rural areas in which almost 80% of the global poor live (Olinto et al., 2013). Thus, agricultural value chains are critical to a country’s growth, as they connect urban consumption with rural production, leading to the emergence of modern consumption patterns, new trends in international trade and impacts on rural areas, spilling over to marketing and production systems (Mango et al., 2015).

Nigeria’s wide range of climate variations allows it to produce a variety of food and cash crops. The staple food crops include cassava, yams, corn, coco-yams, cow-peas, beans, sweet potatoes, millet, plantains, bananas, rice, sorghum, and a variety of fruits and vegetables. The leading cash crops are cocoa, citrus, cotton, groundnuts, palm oil, palm kernel, and rubber. They were also Nigeria’s major exports in the 1960s and early 1970s until petroleum surpassed them in the 1970s (Abayomi, 1997). The import of this narrative is that, over time, the primary product from agriculture was hardly processed before exports, making the country lose the huge potential benefits arising along the value chains (exemplified by such nodes as processing, marketing, distribution, and allied dimensions such as transportation, packaging, storage, financing, insurance, and the like).

The performance of the agricultural sector and its associated value chain has important implications for the achievement of macroeconomic policy objectives (Dlamini et al., 2015). Some of the macroeconomic policies on the agricultural sector adopted in Nigeria from the 1970s include the financial policy where credit to the sector was given at a concessionary interest rate between 1970 and 1985; financial market reforms, which led to the total deregulation of the economy; and the establishment of the Nigerian Agricultural Commerce and Rural Development Ban in 2000 (Evbuomwan et al., 2003). As part of the comprehensive reforms in the financial system and in line with its developmental role, the Central Bank of Nigeria launched the National Micro Finance Policy in 2006. In addition, the Agricultural Credit Support Scheme was established through the initiative of the Federal Government and the Central Bank of Nigeria, with the active support and participation of the Bankers’ Committee. In 2013, an attempt to put an end to institutional problems militating against sustainable growth in the agricultural sector led to the introduction of the Agricultural Transformation Agenda by the Goodluck Jonathan administration. Specifically, the plan aimed to add about 20 million tons of food to domestic supply and create 3.5 million jobs by 2015 (Muftaudeen and Abdullahi, 2014).

Value chain studies have gained considerable importance in recent years. Although many definitions are applied, value chains essentially represent enterprises in which different producers and marketing companies work within their respective businesses to pursue one or more end-markets. The United Nations Industrial Development Organization (2009) defined value chain as the entire range of efforts undertaken to bring products from the initial input-supply stage, through various phases of processing, to its final market destination, and it includes its disposal after use. However, empirical research in Nigeria focused primarily on the link between agricultural output and bank credit. The link between agricultural value chain and monetary and Fiscal factors has rarely been considered. This, therefore, underscores the importance of exploring the role of macroeconomic policy on agricultural value chain in Nigeria.

From the foregoing, the following research questions are expected to be answered in the paper.

-

What are the macroeconomic factors influencing agricultural value chain?

-

What is the impact of macroeconomic policy on agricultural value chain?

Following the introduction, the rest of the paper is structured as follows. Section 2 deals with the literature review. Methodology is covered in Section 3. The estimated results and discussion are dealt with in Section 4. The paper is concluded in Section 5.

2. LITERATURE REVIEW

2.1. Theoretical Framework

The concept of value chains has been defined and described in several ways (Barnes, 2004; Jaffee et al., 2010; Kaplinsky and Morris, 2001; Altenburg, 2006). According to Kaplinsky and Morris (2001. p. 4), value chains are “the full range of activities which are required to bring a product or service from conception through the different phases of production (involving a combination of physical transformation and the input of various producer services), delivery to final consumers, and final disposal after use.” Value chain covers activities such as packaging, storage, transport, and distribution. In other words all value-generating activities, sequential or otherwise vital to the production, delivery and disposal of a product (Schmitz, 2005).

Macroeconomic policy (encompassing Fiscal and monetary policies) is a tool of stabilization and economic growth. Many governments and Fiscal institutions have shown preponderance for Fiscal policies tilted toward high growth and employment (Aurbach, 2004). The macroeconomic objectives of Fiscal and monetary policies include economic growth, price stability, full employment, and sustainable balance of payments. It is expected that an appropriate deployment of Fiscal and monetary policies should bring about price stability, income redistribution, poverty alleviation, and employment generation, and this applies also to agriculture and its allied value chains.

From the foregoing, agricultural value chain and macroeconomic policies are paths in the effort to achieve sustainable economic growth in an economy. Hence, the study of growth has generated a lot of attention among the various schools of thought ranging from the classical to the neoclassical. The Solow-Swan neoclassical growth theory, for example, explains the long-run growth rate of output based on two exogenous variables. The theory concludes that output growth is determined by technical progress and growth in capital and labor inputs. This model provides a few channels for macropolicy influences. Thus, technical progress is assumed to be exogenous and most empirical studies do not suggest that macropolicies have much influence on labor force growth, and hence, it does not matter what the government did (Jhingan, 2010).

This paper benefits from the insights of economic growth models, especially the neoclassical paradigm. Essentially, a reaction to deficiencies found in the Solow-Swan neoclassical growth theory gave rise to the development of endogenous growth theory exemplified by Romer (1986) and Lucas (1988). The theory tries to explain the sustainable or steady growth rate of output based on endogenous factors. The theory recognizes that technological change can be endogenous and that changes in the stock of capital (human and non-human) may generate positive externalities and is not necessarily subject to diminishing returns. The principal motivations of the new growth theory are to explain both growth rate differentials across countries and a greater proportion of the growth observed. In particular, endogenous growth theorists seek to explain the factors that determine the rate of growth of GDP that is left unexplained and exogenously determined in the Solow neoclassical growth equation (the Solow residual). Dar and Amir (2002) pointed out that, in the endogenous growth models, Fiscal policy is very crucial in predicting future economic growth.

Models of endogenous growth bear some structural resemblance to their neoclassical counterparts, but they differ considerably in their underlying assumptions and the conclusions drawn (Moosa, 2002). The most significant theoretical differences stem from discarding the neoclassical assumption of diminishing marginal returns to capital investments, permitting increasing returns to scale in aggregate production, and frequently focusing on the role of externalities in determining the rate of return on capital investments. By assuming that public and private investments in human capital generate external economies and productivity improvements that offset the natural tendency for diminishing returns, endogenous growth theory seeks to explain the role of government (Fiscal policy) in enhancing growth pattern of an economy.

2.2. Empirical Literature

A vast majority of literature links macroeconomic policy to agriculture without actually dealing with value chain. However, such literature is important in an attempt to unravel the role of macroeconomic policy on agricultural value chain. Due to the paucity of literature in this regard, an attempt is made to emphasize the impact of macroeconomic policies on agriculture.

Muftaudeen and Abdullahi (2014) investigated the impact of macroeconomic policies on agricultural output (specifically on crop production) in Nigeria. They applied the vector error correction approach to examine both short-run and long-run relationship over the period of 1978–2011. They found a cointegrating relationship among agricultural output, government expenditure, agricultural credit, inflation, interest, and exchange rates. The findings show that, in the long run, agricultural output is responsive to changes in government spending, agricultural credit, inflation rate, interest rate, and exchange rate. The results of impulse response functions suggest that one standard deviation innovation on government expenditure and interest rate reduces the agricultural output, thus threatening food security in the short, medium, and long terms. Results of the variance decomposition indicate that a significant variation in Nigeria’s agricultural food output is due to changes in exchange rate and government expenditure. The authors recommended that, to achieve a sustainable food security, an expansionary Fiscal policy that is not inflationary should be rigorously pursued along with a realistic exchange rate that takes account of the prevailing internal macroeconomic environment rather than the dynamics of the international undertones.

Dlamini et al. (2015) examined the effect of macroeconomic policies on the agricultural sector in Swaziland, using annual time-series data for the period of 1980–2012. The methodology used is the bound test approach to cointegration. The results revealed that there was a long-run relationship among the variables of agriculture GDP and export. The results also revealed that real money supply, real exchange rate, real GDP, and real government expenditure had a significant long-run impact on agriculture GDP with elasticity coefficients of 0.07, 0.24, 0.88, and −0.3, respectively, while short-run coefficients were −0.002, 0.23, −0.94, and −0.4, respectively. In the case of agricultural exports, the results further revealed that real money supply, real government expenditure, discount rate, real exchange rate, and real GDP had a significant impact on the sector’s exports with long-run elasticity coefficients of 0.13, −0.32, −0.01, 0.5, and 2.53, respectively, while short-run elasticities were 0.06, 0.35, 0.01, 0.46, and −1.34, respectively. The authors recommended that the Central Bank of Swaziland needs to adopt policies aimed to provide affordable credit to agriculture. In terms of the low response of the agricultural sector to macropolicy variables, they recommended that policymakers should intensify the promotion of finished or processed agriculture exports and create a disincentive to imports.

Aroriode and Ogunbdejo (2014) studied the impact of macroeconomic policy on agricultural growth in Nigeria using time-series data from 1970 to 2010, using the ordinary least squares technique. The results show that gross domestic product, credit to agriculture, and exchange rates have significant positive influences on agricultural growth. Income elasticity of agricultural growth was low at 0.939%, indicating the income inelastic nature of agricultural commodities. On the other hand, they found that money supply has an inverse relationship with agricultural production, contrary to expectations. The interest rate is positive but insignificant which can be explained by the restrictive monetary policies, which can cause farm incomes to fall.

Letsoalo and Kirsten (2003) investigated the importance of macroeconomic and trade policies on the agricultural sector in South Africa for the period 1991–1999. According to the authors, macroeconomic and trade policies are determined outside the agricultural sector, and since the 1990s, South Africa has been moving toward deregulation and trade liberalization. Two-stage least squares was the technique used. The results of the study show that 10% reduction in import tariffs will lead to 11.44% increase in the degree of openness of the South African economy. Furthermore, the appreciation of the Rand will raise the domestic prices received by farmers.

Abula and Ben (2016) examined the impact of public agricultural expenditure on agricultural output in Nigeria for the period of 1981–2014. They employed cointegration and Granger causality tests for analysis. The Johansen cointegration test revealed that there was a long-run relationship between agricultural output, public agricultural expenditure, commercial bank loans to the agricultural sector, and interest rates in Nigeria. The results of the parsimonious error correction model showed that public agricultural expenditure has a significant negative impact on agricultural output, while commercial bank loans to the agricultural sector and interest rate have insignificant positive impacts. The researchers, therefore, recommended that monitoring agencies be established by the federal government to ensure that the amount allocated to the agricultural sector is actually and judiciously spent on the sector.

Akpaeti et al. (2014) examined the growth rates in agricultural investments and output in Nigeria from 1970 to 2009 using the ordinary least squares for analysis. Findings revealed that agricultural investments and growth recorded a growth rate of 37.44% and 30.47% in the pre-financial sector reform periods. The result for the financial sector reform periods showed a growth rate of 23.00% and 7.04% for agricultural investment and growth, respectively. The differences in growth rates were not significantly different at 5% between the periods. There was also deceleration in the growth of agricultural investments in the two periods under consideration, implying that financial sector reform might have brought an overall decrease in agricultural investments in the two periods. Furthermore, while there was stagnation in the growth process of agricultural output in the pre-financial sector reform periods, there was an acceleration in the financial sector reform periods. Hence, the researchers suggested that policies and sound regulatory framework that would enhance the development of a strong, healthy, and dynamic financial system should be pursued.

3. METHODOLOGY

3.1. Data Sources and Description of Variables

This paper uses times series data covering 1980–2016, obtained from the World Development Indicators (World Bank, 2017). Our measure of agricultural value chain is agriculture value added as a share of GDP. Although this has certain weaknesses, in that it does not indicate the value at each stage of the agricultural value chain, and it is, however, sufficient for our purpose at the macroeconomic level. Agriculture in this context corresponds to the International Standard Industrial Classification divisions 1–5 and includes forestry, hunting, and fishing, in addition to the cultivation of crops and production of livestock. The value added is the net output of a sector after taking the sum of all outputs and deducting intermediate inputs.

General government final consumption expenditure (as share GDP) was used to capture Fiscal policy; broad money (as share of GDP) was used as a proxy for monetary policy, respectively. Energy supply (electric power consumption kWh per capita) was used as a control variable.

3.2. Model Specification and Estimation Procedure

Value chain aims at producing value-added products or services for a market through the transformation of resources using infrastructures, within the opportunities and constraints of its institutional environment. In this connection, the factors that influence value chain development include market access and market orientation (Grunert et al., 2005), available resources and physical infrastructures (Porter, 1990), and institutions (Scott, 1995).

Factor conditions here deal with a country’s endowment with resources such as physical, human, knowledge, technology, and infrastructure (Porter, 1990). In developing countries, organizations face such challenges as inadequate specialized skills, difficulties in accessing technology, inputs, market, information, credit, and external services (Giuliani et al., 2005). Another key aspect of value chain is the availability of adequate distribution and communication infrastructure, as weak infrastructures hinder the efficient flows of products and exchange of market information. However, emphasis in the paper is the extent to which macroeconomic policies impact agricultural value chain in Nigeria.

In other to capture the impact of macroeconomic policy on agricultural value chain, the following model is specified:

Where AVC represents agricultural value chain; GE denotes government expenditure (Fiscal policy); M2 represents broad money supply (monetary policy); EN denotes energy (a control variable); and µ - the error term, respectively. A priori, Fiscal and monetary policy variables will have a significant positive relationship/impact on agricultural value chain.

In this paper, the autoregressive distributed lag (hereafter ARDL) bounds testing approach (Pesaran et al., 2001) was adopted to examine the macroeconomic policy and agricultural value chain in Nigeria. The advantages that the ARDL framework has over other cointegration methods such as the residual-based technique (Engle and Granger, 1987) and maximum likelihood methods (Johansen, 1988; 1991; Johansen and Juselius, 1990) are well documented (Nyasha and Odhiambo, 2014). According to Akinlo (2006) and Duasa (2007), the ARDL approach does not require pre-testing the variables. However, one needs to be certain that the series employed are not integrated of order 2, in which case, the employment of the ARDL framework becomes devious. To obviate the possibility of using time series data that are integrated of order 2, the stochastic properties of the variables were investigated, using the KPSS (Kwiatkowski et al., 1992), ADF (Dickey and Fuller, 1979), and PP (Phillips and Perron, 1988) tests.

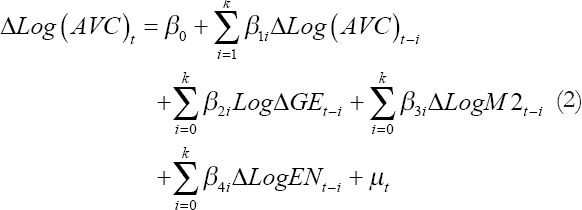

The ARDL model of the specification in Equation 1 is presented as follows:

Where l is the first-difference operator and k is the lag length.

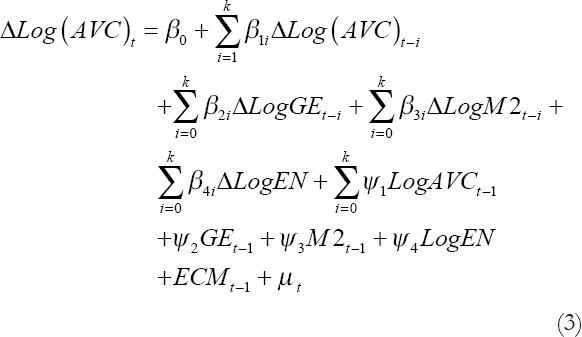

The unrestricted error correction model arising from Equation 2 is specified as follows:

Where the parameters βi: i = 1, 2,…,4 are the short-run dynamic coefficients, the parameters ψi: i = 1, 2,…, 4 are the long-run multipliers, and ECM denotes the speed of adjustment. The post-estimation diagnostics implemented in the paper include the goodness-of-fit, the joint significance of regressors, the serial correlation, and tests for heteroskedasticity, normality, specification error (bias), and stability.

4. RESULTS AND DISCUSSION

4.1. Descriptive Statistics

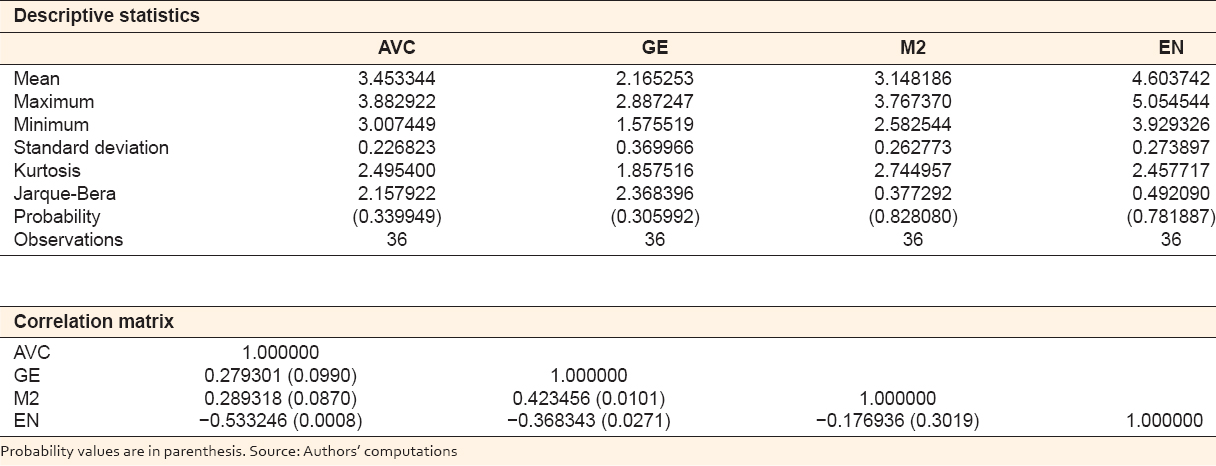

The descriptive statistics of the variables used in the study are presented in Appendix 1. 36 observations were used, and there are four variables in the data set. All the variables are in log form. The data are normally distributed as adjudged from the Jaque-Bera (JB) statistics which is not statistically significant in each case. The kurtosis is reasonably within the required range as none of the values is >3. The correlation matrix indicates that agricultural value chain has a statistically significant positive relationship with government expenditure and money supply and an inverse relationship with energy. Importantly, the independent variables do not exhibit high multicollinearity, the highest correlation coefficient was being 0.42 or 42% between government expenditure and energy.

Appendix 1

4.2. Unit Root TESTS

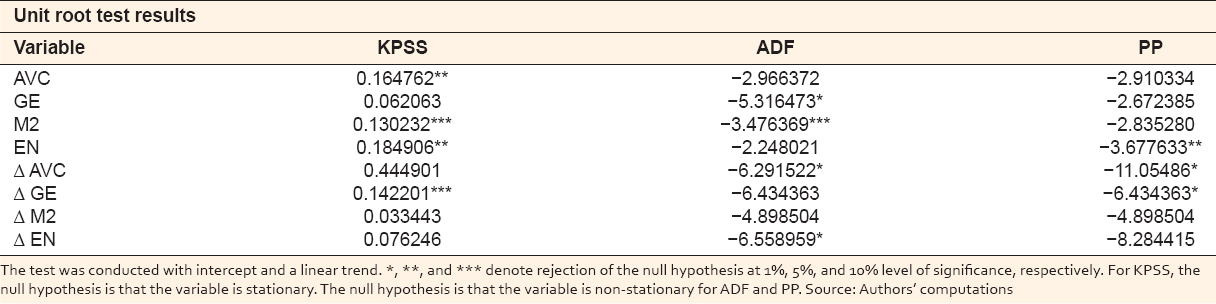

The unit root test results are presented in Appendix 2. The test results indicate that there is a mixture of integration among the variables, a situation that is appropriate for the use of the ARDL approach to cointegration. Consequently, the use of the ARDL bounds test for cointegration is justified, given that none of the variables is integrated of order 2.

Appendix 2

4.3. Cointegration Test

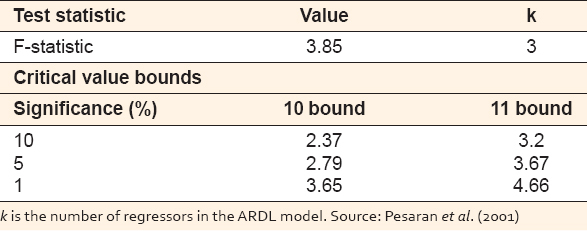

The test of cointegration results is presented in Table 1.

Table 1:Cointegration test results

From Table 1, the computed F-statistics (3.85) is higher than the upper bounds of the critical values at the 5% and 10% levels of significance, respectively. The results suggest that there exists a long-run relationship between agricultural value chain and associated variables employed in the study. It needs to be noted that time series variables are cointegrated if the computed F-statistic is greater than the upper critical bounds value. If the computed F-statistic is lower than the lower critical bounds value, the conclusion is that there is no cointegrating relationship between the variables. If, however, the F-statistic lies between the upper and lower critical bounds values, the results would be inconclusive, and although estimation may proceed, the coefficient of the error correction model should be negative and statistically significant, to resolve the test result in favor of cointegration. It needs to be noted, however, that if cointegration is found, the appropriate step is to implement an error correction model (Engle and Granger, 1987).

4.4. Estimated Coefficients

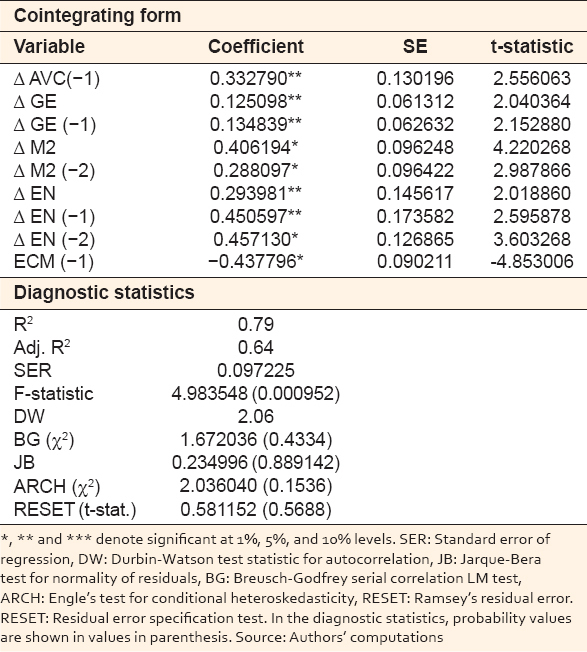

The estimated cointegrating coefficients are presented in Table 2.

Table 2:Estimated coefficients

DISCUSSION

One-lagged value of agricultural value chain exerts a statistically significant positive impact on agricultural value chain output at the 5% level. Thus, past levels of agricultural value chain tend to enhance the current efforts at improvement. This is expected, given that past experience can help bring about the reduction or elimination of errors, consistent with the learning curve theories.

Fiscal policy (captured by government expenditure) has a statistically significant positive impact on agricultural value chain at the 5% level. Both the current and one period-lagged coefficients of government expenditure exert an upward pull on agricultural value chain. Thus, government spending is important to the growth and development of agricultural value chain. Consequently, a 1% rise in government expenditure is associated with a rise in agriculture value chain by about 0.13%.

The monetary policy coefficients (provided by broad money supply) are positively related to agricultural value chain and statistically significant at 1%. In this connection, current and past levels of money supply exert positive influence on agricultural value chain. Thus, changes in the agricultural chain are explainable with recourse to monetary policy initiative. A rise in the current level of money supply by 1% is associated with a corresponding increase in agricultural value added by about 0.41%, while the influence of two-lagged period supply of money impacts agricultural value chain positively by about 0.29%.

All the coefficients of energy (proxied by electricity consumption per capita) are directly related to agricultural value chain and are statistically significant. This implies that higher energy consumption can bring about greater agricultural value added along the value chain. Thus, agricultural value chain can be improved given an improvement in the country’s energy consumption.

The speed of adjustment (i.e., the coefficient of the error correction mechanism) is negative and statistically significant at the 1% level. The sign of the ECM coefficient is consistent with the expectation of theory and is a further validation of the results of cointegration earlier presented in the study. The speed of adjustment indicates that a deviation in agricultural value chain from equilibrium is corrected by about 44% the following year.

The post-estimation diagnostics indicate that about 64% variation (adjusted R2) in agricultural value chain is accounted for by changes in Fiscal and monetary policy variables, in addition to energy consumption. Moreover, the F-statistic indicates that all the regressors employed in the study are jointly statistically significant (at 1%) in explaining changes in agricultural value chain. The Durbin-Watson statistic is in favor of the absence of autocorrelation in the residuals (its value is approximately 2). However, due to the presence of a lagged dependent variable as a regression in the model, the Breusch-Godfrey (BG) statistic is a more appropriate test for the presence or otherwise of autocorrelation. From the estimated results in Table 2, the null hypothesis of no serial autocorrelation is accepted, given the non-statistically significant value of the BG test. Moreover, the residuals in the estimated model are normally distributed, as shown by the JB test statistic which is not statistically significant. Furthermore, the residuals are homoscedastic, as shown by the non-significant ARCH and white test results, respectively. Finally, the model passes the test for specification bias as indicated by the RESET test statistic.

4.6. Stability Tests

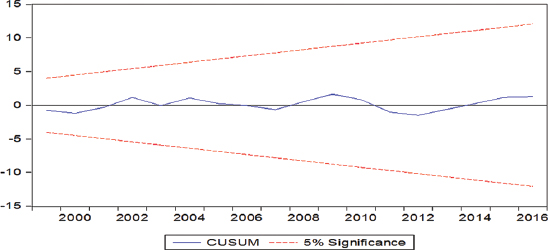

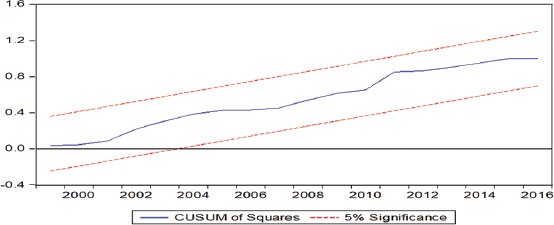

The cumulative sum of recursive (CUSUM) and cumulative sum of the squares of recursive residuals (CUSUMSQ) were used to test the stability of the estimated models. The results are presented graphically in Figures 1 and 2.

Figure 1. Plot of cumulative sum of recursive residuals

Figure 2. Plot of cumulative sum of squared recursive residuals. Source: Authors’ computations

An examination of Figures 1 and 2 indicates that the plots do not cross the 5% critical lines. The implication is that the estimated coefficients within the period of investigation are stable. In other words, there is parameter constancy. Thus, the empirical results would be reliable for policy recommendation.

From the empirical findings and discussion, answers to the research questions posed in the study are provided as follows:

-

The macroeconomic factors influencing agricultural value chain: From the estimated results, government expenditure and money supply are important macroeconomic factors influencing agricultural value chain.

-

The impact of macroeconomic policy on agricultural value chain: The impact of government expenditure and money supply is statistically significant and their impact on agricultural value chain is positive.

5. CONCLUSIONS

The paper investigates macroeconomic policy and agricultural value chain in Nigeria from 1981 to 2016, using the ARDL framework as an analytical tool. A long-run equilibrium relationship was found among the variables used in the investigation. Macroeconomic policy (proxied by government expenditure and broad money supply) was found to have a significant positive impact on agricultural value chain. In addition, energy (captured by electricity consumption per capita) was found to exert a statistically significant positive impact on agricultural value chain.

The conclusion is that macroeconomic policy is critical to agricultural value chain in Nigeria. Consequently, given an enabling macroeconomic policy framework, agricultural value chain can be optimized.

Based on the empirical findings, the following are recommended:

-

Improved government expenditure is advised. In this connection, government budgetary allocation to agriculture needs to be improved and implementation is given a robust impetus. Banks established for the purposes of aiding and promoting agricultural value-added activities (such as the Bank of Industry, the Nigerian Agricultural Commerce and Rural Development Bank, and Small and Medium Enterprises Development Agency of Nigeria) should be strengthened to enhance their capacity to provide funds to agricultural value-added concerns such as processing, storage, marketing, and distribution.

-

Monetary policy should be streamlined in a way that promotes increased money supply to the economy and especially to the real sector, in which agricultural value chain activities tend to be concentrated. Access to dedicated finance to agriculture and its allied value chain activities will go a long way in improving the operations along the value chain.

-

Improved energy supply is required to develop and sustain agricultural value chain in Nigeria. Electricity supply is critical in this respect and falls within the general infrastructural development framework which should be given top priority by governments at all levels. Improvement in electricity can lead to a significant fall in the cost of business operations along the value chain in agriculture, spur growth in agricultural value chain in particular, in addition to reduce waste associated with inadequate storage facilities.

Future investigations of the impact of microeconomic policy on agricultural value chains using cross-sectional or survey data will probably help to shed more light on the microeconomic policy-agricultural value chains nexus.